Now that the Democrats control the House, Senate, and the White House, you’re probably wondering what the new administration means for your tax bill—and your portfolio.

There’s good news here, and it comes in two parts: first, the tax hit likely won’t be as much as you think (if you notice it at all!). And second, Biden’s tax plan has quietly boosted the municipal-bond market, where there are scores of tax-free dividends waiting for us. And it’ll likely boost it even more in the months ahead.

First Up, Your Tax Bill

The takeaway is that, while there are some changes in the tax code in Biden’s latest plan, taxes will remain lower than they were when President Trump first took office. Biden’s increases from Trump’s 2017 tax cuts are marginal and will have barely noticeable effects on most Americans.

Biden’s Tax Plan Highlights

- Raise taxes on incomes above $400,000, including 12.4% Social Security payroll tax.

- Raise corporate income tax from 21% to 28%.

- 0.6% to 10.8% after-tax-income gains for taxpayers in 0% to 80% tax brackets in 2021.

- Less than 1% decline in after-tax income for taxpayers in 0% to 95% tax brackets over the long run.

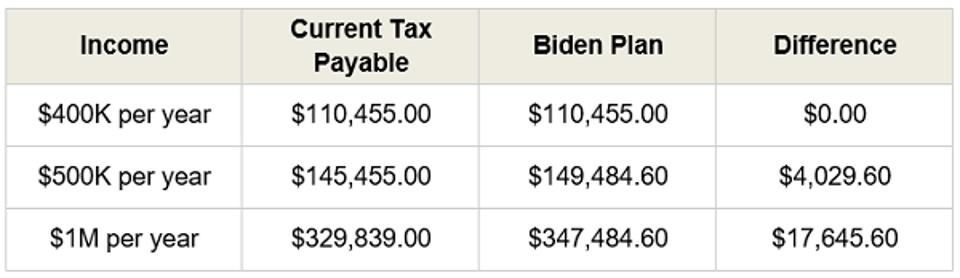

There are a couple of important implications for investors, however, and they’re effects of Biden’s attempts to target taxes on the 1%. As a result, income earners who make more than $400,000 could see their overall tax burden rise by a few thousand dollars per year.

Bear in mind that you have to earn a lot more for this to kick in. Since these are marginal tax rates, that tax bump only applies to income earned above $400,000. That means you really need to earn a lot more than $400,000 for the tax changes to be noticeable.

Tax Changes: Really Only Noticeable at $500K a Year

In fact, for your tax burden to rise by $12,000 per year, you need to be making $800,000—meaning the total tax hike for someone earning that much is just 1.5% of their total income. A bit of a sting, to be sure, but not debilitating.

This is by design. Biden’s tax plan is aimed at wealthy individuals: think investment bankers, high-flying corporate lawyers, and the like. These people also tend to live in highly taxed jurisdictions (think California, New York, and New Jersey), which also means they’ll suddenly have an even bigger incentive to find tax advantages where they can.

Which leads me to …

Our Opportunity for Biden-Driven Upside (and Tax-Free Dividends)

If you’re one of these high-six-figure earners in a high-tax state, there’s really only one place you can go to avoid taxes: municipal bonds.

If you aren’t familiar with them, “muni” bonds are a kind of debt that organizations from hospitals to state governments take out by issuing bonds that are then sold on the public market, usually to big institutional investors, as well as wealthy individuals.

(But as I’ll show you shortly, regular folks can also access them through a closed-end fund [CEF]. Like stocks and ETFs, CEFs can be bought and sold on the stock market at any time during regular trading hours.)

To encourage investors to buy, federal (and many state) governments waive taxes on the income these bonds pay out, meaning muni bonds give you an income stream that increases your cash flow without increasing your tax bill.

If you’re a lawyer making $400,000 and you can get $100,000 in income from tax-free municipal bonds rather than, say, taxable dividend-paying stocks, this (legal) opportunity to grab tax-free payouts is a big deal. This is why the muni-bond market jumped when Biden’s victory became apparent shortly after Election Day, and munis have stayed relatively high since then.

A 1.9% move might not seem like very much—and with the stock market, for example, it wouldn’t be—but it’s a big jump for a market as stable as municipal bonds.

This, in turn, has been great for the iShares National Municipal Bond ETF (MUB), an index fund that tracks this market. But it’s been even better for muni-bond CEFs like the PIMCO Municipal Income II Fund (PML), which trades in the same market but has spiked even further.

One of the biggest reasons for this is that muni-bond CEFs out-yield the index fund while still being tax-free (in most cases); while MUB yields 2.2% tax-free, PML’s tax-free yield is an impressive 5%. Plus, PML has been outperforming the index fund ever since both have existed.

Michael Foster is the Lead Research Analyst for Contrarian Outlook. For more great income ideas, click here for our latest report “Indestructible Income: 5 Bargain Funds with Safe 8.3% Dividends.”

This article was legally licensed through AdvisorStream